Cyber threats are hitting businesses harder than ever, with cyber incidents threatening to bankrupt small companies overnight. Most people think big corporations are the main targets since they have more data and deeper pockets. But actually, small and medium-sized businesses face even greater risks because they lack expensive protection and a single breach can wipe them out completely.

Table of Contents

- What Is Cyber Insurance And What Does It Cover?

- The Importance Of Cyber Insurance For Small And Medium-Sized Businesses

- How Cyber Insurance Works In The Face Of Cyber Threats

- Key Concepts And Terms In Cyber Insurance Explained

- Real-World Examples Of Cyber Insurance In Action

Quick Summary

| Takeaway | Explanation |

|---|---|

| Cyber insurance mitigates financial risks. | It offers businesses financial protection against losses from cyber incidents like data breaches and ransomware attacks. |

| First-party and third-party coverage are essential. | First-party covers your own losses, while third-party addresses claims against your business, providing comprehensive protection. |

| Small businesses are increasingly targeted by cybercriminals. | Lack of robust cybersecurity makes smaller organizations vulnerable, highlighting the need for specialized insurance. |

| Understanding insurance terms is crucial. | Familiarity with key concepts like coverage triggers and risk transfer helps businesses choose the right policy. |

| Cyber insurance supports recovery and future prevention. | It provides not just financial reimbursement, but also access to expertise for risk management and incident response. |

What is Cyber Insurance and What Does It Cover?

Cyber insurance is a specialized type of business protection designed to help organizations mitigate financial risks associated with digital threats and data breaches. Unlike traditional insurance policies, cyber insurance addresses the unique challenges businesses face in an increasingly interconnected technological landscape.

Understanding Cyber Insurance Fundamentals

Cyber insurance provides financial protection against losses resulting from cyber incidents like data breaches, network security failures, and digital attacks.

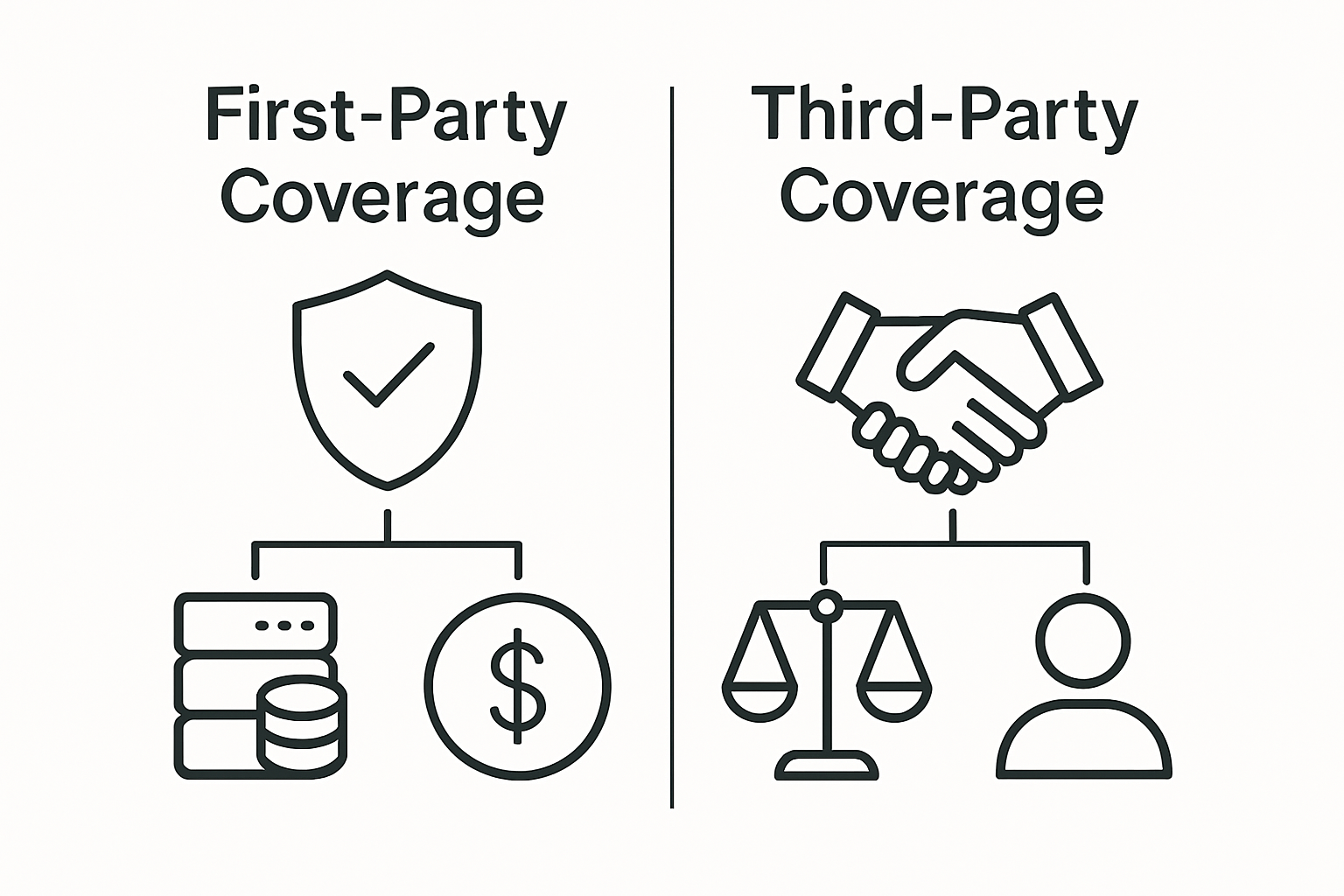

According to the Federal Trade Commission, these policies typically cover both first-party and third-party risks.

According to the Federal Trade Commission, these policies typically cover both first-party and third-party risks.

First-Party Coverage protects your own business by covering direct expenses such as:

- Forensic investigation costs

- Data recovery expenses

- Business interruption losses

- Cyber extortion and ransom payments

- Customer notification and credit monitoring services

Third-Party Coverage addresses potential legal and financial consequences from claims made against your organization, including:

- Legal defense costs

- Regulatory fines and penalties

- Settlement expenses

- Liability claims from affected customers or partners

Types of Cyber Incidents Typically Covered

A comprehensive cyber insurance policy generally includes protection against multiple digital threats. These might encompass:

- Ransomware attacks

- Phishing and social engineering scams

- Unauthorized network access

- Data theft and breach incidents

- Accidental data loss or system failures

Businesses should carefully review policy details, as coverage can vary significantly between insurance providers. Work closely with an experienced insurance professional who understands your specific industry and technological infrastructure to design a tailored cyber insurance strategy that addresses your unique risk profile.

Below is a comparison table outlining the differences between first-party and third-party cyber insurance coverage to help clarify which risks each type addresses.

| Coverage Type | Who/What It Protects | Examples of Covered Expenses |

|---|---|---|

| First-Party Coverage | Your own business and direct losses | Forensic investigation, data recovery, business interruption, ransom payments, customer notifications |

| Third-Party Coverage | Claims and actions by external parties | Legal defense, regulatory fines, settlements, liability claims from customers or partners |

The Importance of Cyber Insurance for Small and Medium-Sized Businesses

Small and medium-sized businesses are increasingly becoming prime targets for cybercriminals, making cyber insurance a critical component of modern business risk management. Unlike large corporations with extensive IT resources, smaller organizations often lack robust cybersecurity infrastructure, making them more vulnerable to digital threats.

Financial Vulnerability in the Digital Landscape

According to the National Institute of Standards and Technology, small businesses represent 99.9% of all firms and are particularly susceptible to cyber attacks that can cause devastating financial consequences. Cyber incidents can quickly escalate into existential threats, potentially bankrupting businesses that are unprepared to manage substantial recovery costs.

Key Financial Risks for Small Businesses Include:

- Immediate breach response and investigation expenses

- Data recovery and system restoration costs

- Potential legal and regulatory penalties

- Lost revenue during business interruption

- Potential permanent loss of customer trust

Strategic Protection Beyond Traditional Insurance

Cyber insurance offers more than financial reimbursement. It provides comprehensive support mechanisms that help businesses navigate complex digital security challenges. These policies often include:

- Proactive risk assessment services

- Incident response planning

- Access to cybersecurity experts

- Legal and regulatory compliance guidance

- Technical support during and after a cyber incident

For small and medium-sized businesses, cyber insurance is not just a financial safety net but a strategic investment in long-term resilience. By transferring potential digital risks and providing expert support, these policies enable organizations to focus on growth while maintaining robust protection against evolving cyber threats.

How Cyber Insurance Works in the Face of Cyber Threats

Cyber insurance operates as a sophisticated risk management mechanism designed to provide financial protection and strategic support when businesses encounter digital security challenges.

Unlike traditional insurance products, these policies are dynamically structured to address the complex and rapidly evolving landscape of cyber threats.

Policy Activation and Response Mechanisms

According to the National Conference of State Legislatures, cyber insurance policies are triggered when specific cyber incidents occur. The claim process involves several critical stages that help businesses navigate potential financial and operational disruptions:

- Immediate incident reporting and documentation

- Forensic investigation to determine breach extent

- Assessment of potential financial and operational impacts

- Coordinating response strategies with insurance providers

- Implementing recovery and mitigation measures

Coverage Scope and Financial Protection

Cyber insurance policies typically encompass a comprehensive range of financial protections designed to shield businesses from the multifaceted consequences of digital security breaches. Key coverage areas include:

- Direct financial losses from cyber attacks

- Expenses related to data recovery and system restoration

- Legal fees and regulatory compliance costs

- Business interruption compensation

- Public relations and reputation management expenses

The effectiveness of cyber insurance depends not just on financial reimbursement but on providing holistic support. Insurers often collaborate with cybersecurity experts to help businesses prevent future incidents, offering risk assessment services, security recommendations, and proactive threat monitoring. This approach transforms cyber insurance from a reactive financial tool into a strategic partnership for digital resilience.

Key Concepts and Terms in Cyber Insurance Explained

Cyber insurance introduces a complex set of specialized terminology that can be challenging for businesses to navigate. Understanding these key concepts is crucial for making informed decisions about digital risk protection and selecting appropriate coverage strategies.

Core Insurance Terminology

According to the U.S. Government Accountability Office, cyber insurance encompasses several fundamental terms that define policy structure and protection mechanisms. Critical foundational concepts include:

- Coverage Triggers: Specific events or conditions that activate insurance protection

- Aggregate Limits: Maximum total amount an insurer will pay across all claims

- Endorsements: Modifications or additions to standard policy terms

- Risk Transfer: Shifting potential financial losses from the business to the insurance provider

- Underwriting: Process of evaluating and pricing potential cyber risks

Advanced Policy Definitions

Specialized cyber insurance terms provide deeper insights into policy mechanics:

- First-Party Coverage: Direct protection for the insured organization’s own losses

- Third-Party Coverage: Protection against claims and legal actions from external parties

- Retroactive Date: The earliest point from which continuous coverage is maintained

- Incident Response Coverage: Expenses related to managing and mitigating a cyber event

- Business Interruption Protection: Compensation for revenue losses during system downtime

Effective cyber insurance requires businesses to thoroughly understand these terms, ensuring they select policies that provide comprehensive protection tailored to their specific technological infrastructure and risk profile. By mastering these concepts, organizations can develop more strategic approaches to digital risk management and financial security.

The following table defines key cyber insurance terms mentioned in the article, enabling easier understanding of core policy concepts and terminology.

| Term | Definition |

|---|---|

| Coverage Triggers | Specific events or conditions that activate insurance protection |

| Aggregate Limits | Maximum total amount an insurer will pay across all claims |

| Endorsements | Modifications or additions to standard policy terms |

| Risk Transfer | Shifting potential financial losses from the business to the insurance provider |

| Underwriting | Process of evaluating and pricing potential cyber risks |

| Retroactive Date | The earliest point from which continuous coverage is maintained |

| Incident Response Coverage | Expenses related to managing and mitigating a cyber event |

| Business Interruption Protection | Compensation for revenue losses during system downtime |

Real-World Examples of Cyber Insurance in Action

Cyber insurance transforms from an abstract concept to a critical business lifeline when real-world scenarios demonstrate its practical value. These practical examples illustrate how cyber insurance can mean the difference between business survival and total financial collapse during digital emergencies.

Small Business Ransomware Recovery

According to the U.S. Government Accountability Office, cyber insurance has become increasingly vital in managing digital risks. A compelling example involves a mid-sized manufacturing company that experienced a sophisticated ransomware attack. Without cyber insurance, the potential financial impact would have been catastrophic:

- Initial ransom demand: $250,000

- Forensic investigation costs: $50,000

- System restoration expenses: $75,000

- Business interruption losses: $100,000

- Legal and compliance fees: $25,000

Their cyber insurance policy covered approximately 80% of these expenses, enabling the business to recover quickly without facing potential bankruptcy. The insurance not only provided financial reimbursement but also connected the company with cybersecurity experts who helped prevent future incidents.

Healthcare Data Breach Scenario

Another instructive scenario involves a regional healthcare provider confronting a significant patient data breach. The incident exposed sensitive medical records, triggering complex legal and regulatory challenges:

- Patient notification expenses

- Credit monitoring services for affected individuals

- Regulatory compliance penalties

- Potential lawsuit defense costs

- Reputation management and public relations

In this instance, the cyber insurance policy’s comprehensive third-party coverage was instrumental in managing the multifaceted consequences of the data breach. The provider avoided potentially ruinous financial penalties and maintained patient trust through prompt, professional incident response.

Protect Your Business from Cyber Threats with Local Experts

Cyber attacks are a real risk for small and medium-sized businesses. As the article on cyber insurance explains, the costs of data breaches, ransomware, and business interruption can cripple your operations. Many organizations are left struggling with financial losses, compliance headaches, and damage to customer trust. If your current IT resources fall short or you worry about gaps in your digital defenses, you are not alone. Protecting sensitive data and keeping your company running safely has never been more critical.

Now is the time to partner with a team that understands the challenges outlined in the article, such as risk transfer, compliance, and full-coverage cybersecurity. At SRS Networks, we provide proven cybersecurity solutions and business continuity support to guard against digital disruptions. Let us help you build resilience and secure peace of mind so you can focus on growing your business. Reach out today to start a conversation about customized IT protection for your needs.

Frequently Asked Questions

What is cyber insurance?

Cyber insurance is a specialized type of business protection that helps organizations mitigate financial risks associated with digital threats and data breaches. It covers expenses related to cyber incidents and provides support during recovery.

What does cyber insurance typically cover?

Cyber insurance usually offers coverage for first-party risks like forensic investigation costs, data recovery expenses, and business interruption losses, as well as third-party risks such as legal defense costs and regulatory fines.

Why is cyber insurance important for small businesses?

Cyber insurance is critical for small businesses because they are increasingly targeted by cybercriminals and often lack robust cybersecurity measures. This insurance helps protect against financial ruin from unexpected cyber incidents.

How do businesses activate their cyber insurance policy after an incident?

To activate their policy, businesses need to report the cyber incident immediately, document the events, undergo a forensic investigation, assess the impact, and coordinate recovery strategies with their insurance provider.